Spectrum Valuation ($SATS) - Part 3

Part 3 of a multi-part series on the economics of spectrum and EchoStar’s spectrum portfolio

Today we will focus on EchoStar’s 700MHz block.

700MHz Block

1 x 6 Mhz (unpaired)

722-728 MHz Bands

History

In 2008, EchoStar used a wholly-owned subsidiary, Frontier Wireless LLC, to participate in Auction 73, a blockbuster auction of the 700MHz block that raised $19.6B in total proceeds. The biggest winners in this auction were Verizon and AT&T, with 83% of winning bids. Sprint and T-Mobile did not buy any spectrum in this auction.

The auctioned spectrum was divided into 5 blocks. Echostar only bought a piece of the E-block.

The A-block was a paired 6MHz spectrum with no restrictions. However, there were some interference concerns with TV channels adjacent to this spectrum. The average price per MHz-POP was $1.16. Verizon and U.S. Cellular took this block down.

The B-block was also a paired 6MHz spectrum with no restrictions and no interference issues. Verizon and AT&T both took large pieces of this block. AT&T only focused on the B-block in this auction. U.S. Cellular also participated in this block. The average price per MHz-POP was $2.67.

The C-block was a paired 11MHz spectrum, but had some open access mandate, which reduced the final transaction price. Verizon took down most of the C-block with an average price per MHz-POP of $0.76.

The D-block was a paired 5MHz spectrum with sharing obligations. There were no qualified bids on this block.

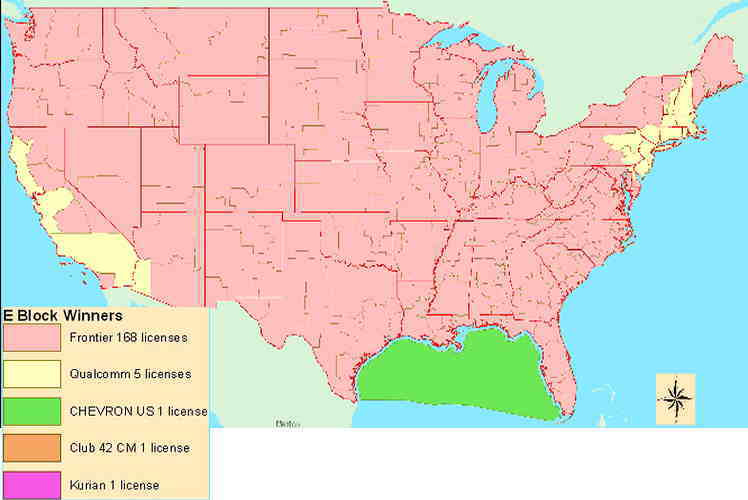

The E-block was an unpaired 6MHz spectrum that EchoStar and Qualcomm bought. EchoStar focused on the smaller markets and paid $712M to purchase 168 licenses (1.532B MHz-POP) for an average price of $0.46 per MHz-POP. Because this spectrum was unpaired, EchoStar was probably planning to use it to stream TV shows. Qualcomm paid $555M for its E-block licenses to use in its MediaFlo business (streaming TV).

Below is a map of Echostar (Frontier Wireless LLC)’s 700MHz E-block licenses.

Currently the 700MHz E-block is used by EchoStar as a supplemental downlink layer (Band n29) in its network, in combination with Bands 71, 66 and 70.

The 700MHz E-block was unencumbered until 1Q 2025, when EchoStar substituted a small portion of its 3.45GHz licenses with these 700MHz licenses as collateral for the DDBS intercompany loan. Currently, this block, along with the bulk of the 3.45GHz license portfolio and other smaller pieces, is collateral for this $7.5B intercompany loan.

Compliance of Build-out Requirements

The initial build-out requirements mandated that DISH provide signal coverage and offer service to at least 35% of the geographic area within each license area by June 13, 2013. Failure to meet that benchmark would have triggered an accelerated final deadline and potential loss of license. In September 2013, DISH requested modifications to the build-out schedule, proposing instead a new framework: 40% population coverage by 2017 and 70% by 2021, arguing for alignment with its broader spectrum deployment strategy including AWS-4. These requests were not adopted as originally proposed, but the matter remained open as DISH continued to accumulate other spectrum assets and delay its wireless rollout.

Following DISH’s acquisition of Boost Mobile and commitments made to the FCC and DOJ in connection with the Sprint/T-Mobile merger in 2019, the FCC issued an order in September 2020 that significantly revised DISH’s build-out obligations across multiple bands, including the 700 MHz E-Block. The revised requirement stipulated that DISH must provide 5G broadband service to at least 70% of the population in each economic area covered by its licenses by June 14, 2023.

In 2024, DISH requested and received an extension from the Wireless Bureau that pushed out the compliance date to December 2026, with a further extension to June 2028, conditional upon meeting public interest commitments such as:

Achieve 80% population coverage with Boost Mobile by December 2024 and accelerate and expand milestones for over 500 licenses,

Deploy 24K towers by June 2025,

Offer $25/30GB low-cost plan, and

Provide spectrum-leasing access to Tribal and small carriers.

Based on FCC filings, it looks like 71% of the 700MHz licenses has met the 80% coverage threshold.

Spectrum Characteristics

The 700MHz E-Block is a 6MHz downlink-only block paired with no uplink spectrum. This block is typically used as supplemental downlink (SDL) in LTE/5G deployments (Band n29 for 5G NR), enhancing capacity for video and other downstream-heavy traffic. It offers excellent propagation characteristics, long range and strong building penetration, similar to other low-band spectrum.

In contrast, other 700MHz blocks, particularly the Lower A, B, and C Blocks (698–716 MHz for uplink and 728–746 MHz for downlink), are paired, offering 2x6 MHz or 2x5 MHz channels ideal for two-way mobile service. These were more actively deployed by carriers like AT&T and Verizon in the early 2010s. Verizon, for instance, built its nationwide LTE network on the Upper C Block (746–757 MHz / 776–787 MHz), which includes a broader 2x11 MHz channel and an open access provision. These paired blocks are more flexible and foundational for primary LTE/5G coverage layers due to their ability to handle both uplink and downlink traffic.

Compared to the 600MHz band (auctioned in 2017), the 700MHz spectrum sits slightly higher in frequency but exhibits similar propagation behavior. See Part 2 of this series for details on the 600MHz band.

Recent Valuation Comparables

AT&T bought Qualcomm’s lower 700MHz D&E blocks (Feb 2011)

In December 2010, Qualcomm agreed to sell its Lower 700MHz D and E-block spectrum licenses to AT&T for $1.925B, covering over 300M people in the US. This included 12 MHz in major metro areas (e.g., New York, LA) and 6 MHz elsewhere. AT&T intended to use the spectrum as supplemental downlink (SDL) via carrier aggregation, aiming to bolster LTE capacity and indoor coverage. Qualcomm bought the E-block alongside Echostar in 2008. The D-block was purchased by Qualcomm years earlier for very little money. The price per MHZ-POP was estimated at $0.85 for the whole transaction. We don’t have a breakout for just the E-block piece.

T‑Mobile purchased Verizon’s entire A-block portfolio (Jan 2014)

Verizon agreed to sell its lower 700MHz A-block spectrum to T-Mobile for $2.365B in cash. The deal also includes the swapping of AWS and PCS spectrum licenses from T-Mobile to Verizon, with a total estimated value of approximately $950 million. T-Mobile paid $1.85 per MHz-POP (vs. Verizon’s acquisition price of $1.47 in 2008).

AT&T/Verizon Spectrum Swap (Jan 2013)

Verizon agreed to sell a huge chunk of its Lower 700MHz B-block spectrum to AT&T for $1.9 billion. Under the deal, Verizon will sell 39 lower 700MHz B-block licenses to AT&T in exchange for a payment of $1.9 billion and the transfer by AT&T to Verizon of 10MHz AWS licenses in certain western markets, including Los Angeles, Phoenix, Fresno, Calif., and Portland, Ore. AT&T paid $4.29 per MHz-POP for Verizon’s B-block.

T-Mobile bought U.S. Cellular Assets (Oct 2024)

T-Mobile’s proposed acquisition of U.S. Cellular’s assets includes 700MHz A-block spectrum, which T-Mobile says it can put to use almost immediately after closing the deal, and at virtually no cost because these holdings are in spectrum bands supported by existing radios.

AT&T acquired 3.45GHz and 700MHz B/C-blocks from U.S. Cellular (Oct 2024)

AT&T struck a deal with U.S. Cellular to acquire 1.25 billion MHz‑POPs of 3.45 GHz mid-band spectrum and an additional 331 million MHz‑POPs of 700 MHz B/C-block licenses for $1.018 billion in cash. We don’t have a breakout of the prices paid for each block.

Verizon purchase U.S. Cellular 850MHz licenses (Oct 2024)

Verizon bought 663M MHz-POPs of U.S. Cellular’s 850MHz spectrum licenses as well as 11M MHz-POPs of its AWS and 19M MHz-POPs of its PCS licenses for a total of $1 billion. The average price is approximately $1.50 per MHz-POP.

Potential Bidders

DISH's 700 MHz E-block spectrum is a niche asset. Its most likely buyers would be wireless operators seeking supplemental downlink (SDL) to relieve network congestion, especially in high-traffic areas. AT&T stands out as the most logical acquirer, given its existing deployment of Band 29 (which corresponds to the 700MHz E-block), ecosystem support in devices, and historical precedent ($1.925 billion acquisition of Qualcomm's D and E block licenses in 2011).

T-Mobile may also have interest. T-Mobile already anchors its low-band 5G on 600 MHz (Band 71), but they bought 700MHz A-block, with the download link adjacent to the E-block. E-block for them might only be regionally useful, likely in dense urban areas where unpaired downlink helps offload data. Verizon historically has only shown interest in its own 700MHz C-block licenses.

Charter and Comcast would not be interested due to the block’s narrow bandwidth, lack of uplink, and fragmented ownership patterns, making it most attractive as a complementary asset rather than a foundational one.

My Valuation

I think the range of reasonable valuation for DISH’s 700MHz E-block is $0.65-$1.00 per MHz-POP. I assigned the bottom of the range for my valuation due to the uniqueness and limited usage of this slice. Remember that DISH’s E-block licenses exclude large metro areas in the NorthEast and West Coast. The valuation comparables are imperfect. The total market value of this block is estimated at $1B. Could the valuation be even lower? Unlikely, given that the initial auction was 17 years ago at $0.46 per MHz-POP and secondary asset values in the 700MHz block have gone up.

My Key Takeaways

The key takeaways for DISH’s 700MHz E-block are:

Small slice with limited usage due to lack of uplink spectrum. Act in a supporting manner and only valuable to the 3 carriers.

It’s got national coverage outside of Boston, NYC, LA, Philly and SF.

AT&T and T-Mobile are likely bidders. But not meaningful for either of them.